"

"

Key Takeaways

- In stark contrast to trends observed for homeowners under age 65, mortgage use among homeowners age 65-plus has risen steadily in recent years.

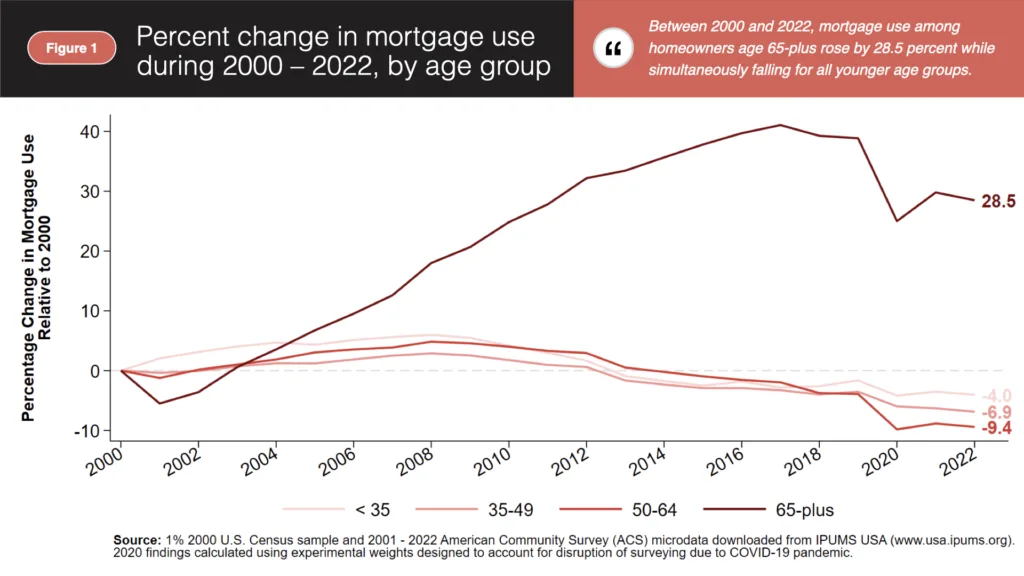

- Between 2000 and 2022, mortgage use by homeowners age 65-plus rose by 28.5 percent.

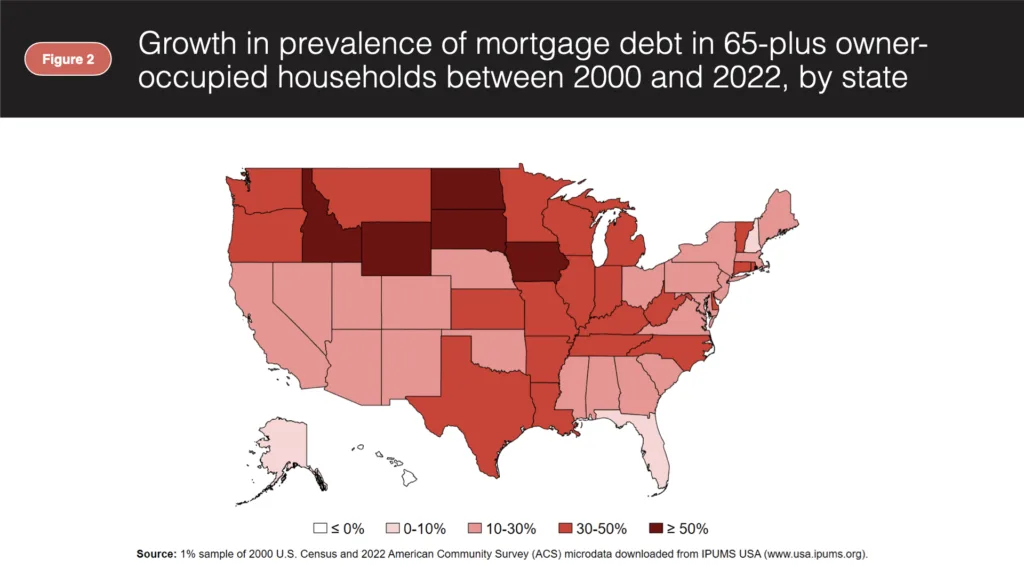

- The use of mortgages among older homeowners is rising almost everywhere, but the extent of this rise varies dramatically by state.

- It is imperative that policymakers and business leaders develop policies and practices that promote an equitable mortgage market that fosters affordable homeownership and economic security for every generation.

Contrary to their younger counterparts, American homeowners1 over age 65 are increasingly using mortgages2. This development is not bad in and of itself, but it does raise critical issues for policymakers and business leaders, particularly relating to the elevated rejection rates and higher borrowing costs that older adults face in the mortgage market. Understanding and addressing these challenges will be central to fostering a market that provides fair and equitable access to mortgages for people of every age.

Mortgage debt remains uncommon among homeowners age 65-plus relative to their younger counterparts; in fact, the fraction of homeowners age 65-plus who had a mortgage in 2022 (34 percent) was less than half that of homeowners under age 65 (70 percent)3. However, trends in mortgage use among older and younger homeowners have diverged for many years4. Between 2000 and 2022, mortgage use among homeowners age 65-plus rose by 28.5 percent while simultaneously falling for all younger age groups. This rise reached a peak in 2017, when mortgage use among 65-plus homeowners was 41.1 percent higher than its 2000 level. The COVID-19 pandemic drove a significant decline in mortgage use among 65-plus homeowners in 2020, but more recent data suggest that mortgage use among older homeowners is rising once again.

Between 2000 and 2022, mortgage use among 65-plus homeowners rose almost everywhere5, but the scale of this growth varied dramatically from state to state. Mortgage use among older homeowners grew by less than 10 percent in Florida, New Hampshire, and Alaska; meanwhile, five states (Wyoming, South Dakota, North Dakota, Iowa, and Idaho) saw increases of over 50 percent. The forces driving this variation are complex; however, there is clear evidence that growth in mortgage use among 65-plus homeowners was especially strong in certain regions of the country (e.g., the Midwest).

Rising mortgage use among older homeowners is not necessarily a bad development; for example, a mortgage can serve as a cost-effective tool for accessing home equity6. However, as older homeowners come to rely on mortgage products more, it is critical that this population is well-informed about their options, and that policies and practices in the mortgage market meet the needs of every generation. These necessities are underscored in a 2023 working paper by Natee Amornsiripanitch7, which finds that older adults face significantly higher application rejection rates and borrowing costs in the mortgage market. Age discrimination may partly explain these negative outcomes; however, several factors are likely to play a role8. Whatever the cause, these disparities can have serious economic consequences, including lower economic security among older homeowners who are unable to access wealth stored as home equity.

AARP closely follows research examining housing issues important to older adults. In April 2023, AARP published an online article that covers Amornsiripanitch’s findings and highlights proactive steps that older adults and lenders can take to close mortgage deals with fair terms. One striking example covered in the article is that mortgage applications submitted by older adults are commonly denied because of an incorrectly calculated debt-to-income (DTI) ratio9. This can happen because loan officers are used to underwriting mortgages based on earned income, since this source represents the vast majority of income for a typical (i.e., younger) mortgage applicant. Given that older adults commonly receive a substantial fraction of their income via other sources (e.g., investment income, social security), a full accounting of these income streams is necessary for a lender to accurately assess the applicant’s ability to afford the mortgage10.

This article is just one example of AARP’s efforts to inform older consumers about their options with respect to mortgages; other recent articles examine reverse mortgages and the pros and cons of paying off a mortgage before retirement. In addition, AARP champions public policies and business practices that ensure equitable access to mortgages for people of every generation, strong consumer protections, and flexible loan servicing policies that allow homeowners to retain their homes during periods of financial stress. In an environment where older adults are increasingly turning to mortgages, efforts of this kind are central to creating an equitable mortgage market that fosters affordable homeownership and economic security for every generation.

- In the context of this article, a “homeowner” is defined as a householder who owns their home. In the U.S. Census and American Community Survey (ACS), a “householder” is the person (or one of the people) in whose name the household is owned or rented. In cases where the household is jointly held by more than one person (e.g., a married couple), the householder may be any member of that set. For more information, see the “Household Type and Relationship” section beginning on page 82 of the 2022 ACS/PRCS Subject Definitions. ↩︎

- For the purposes of this article, a homeowner is said to be “using” a mortgage if at least one form of debt is held against their physical household. This includes traditional mortgages, as well as other debt instruments such as reverse mortgages. The homeowner’s specific motivation for using a mortgage is not explicitly covered in the ACS; the typical purpose of a mortgage is to finance the purchase of a home; however, mortgages can be used for other purposes (e.g., someone who owns their home outright may use a mortgage to access home equity). A single property can have multiple mortgages. ↩︎

- According to 2022 American Community Survey (ACS) public-use microdata downloaded from IPUMS USA (www.usa.ipums.org). ↩︎

- Notably, mortgage use among 65-plus homeowners has been rising for a considerably longer period of time; in fact, Collins, Hembre, and Urban (2020) show that this trend extends back to at least 1980. ↩︎

- Mortgage use among 65-plus homeowners fell slightly in Hawaii and the District of Columbia during 2000 – 2022.

↩︎ - Recent research suggests that low interest rates are one of several factors responsible for rising mortgage use among older homeowners. Collins, Hembre, and Urban (2020) discuss these factors and their potential role. ↩︎

- Dr. Amornsiripanitch is a senior financial economist at the Federal Reserve Bank of Philadelphia. ↩︎

- For example, age-related mortality risk makes it more costly (on average) for lenders to give mortgages to older homeowners, a fact that may contribute to higher rejection rates and borrowing costs for this population. A February 2023 article from the Center for Retirement Research at Boston College reviews Amornsiripanitch’s findings and potential explanations in detail. ↩︎

- This example is provided by Brian Rugg, Chief Credit Officer at LoanDepot. ↩︎

- If sizable income streams are excluded, an applicant’s debt will appear large relative to their income (i.e., a high DTI ratio). This may lead the lender to incorrectly conclude that the applicant cannot afford the mortgage. ↩︎